U.S and Michigan Economy Webinar

On Tuesday, February 28, I hosted a 30-minute webcast on the current state of the U.S. and Michigan economies. This blog provides a summary of the webcast.

A year-over-year comparison of some main economic indicators for the U.S. economy (table 1) shows that the U.S. economy continued to expand in 2016 at a moderate pace and labor markets continued to improve, but inflation remained below the Federal Open Market Committee’s 2% longer-run objective.

Table 1: U.S. Main Economic Indicators

| Indicator | 2014 | 2015 | 2016 |

| Gross Domestic Product 1 | 2.4% | 2.6% | 1.6% |

| Unemployment Rate 2 | 6.2% | 5.3% | 4.9% |

| Participation Rate 2 | 62.9% | 62.7% | 62.8% |

| Nonfarm Job Growth 3 | 2,558 | 2,876 | 2,493 |

| PCE Core Inflation 4 | 1.6% | 1.4% | 1.7% |

- Year-over-year

- Annual Average

- Annual Average Employment – Y/Y Change in thousands

- Annual Average PCE Core Inflation – Percent Change Y/Y

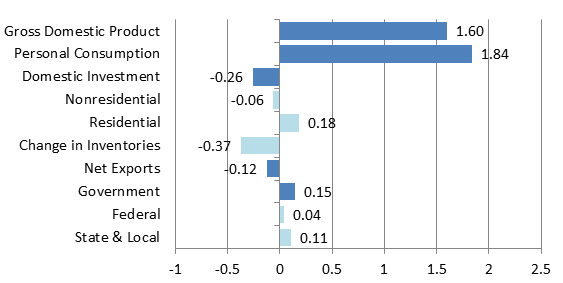

Consumer spending (personal consumption growth in chart 1) made the largest contribution to U.S. economic growth in 2016. Improved labor conditions and growing personal income facilitated U.S. consumers’ ability to purchase U.S. goods and services. Consumers contributed 1.8% to total GDP growth of 1.6% for the year. Total GDP growth ended up lower because of negative contributions from gross private domestic investment and net exports. While domestic residential investment added 0.2%, offsets from nonresidential (-0.1%) and inventory investment (-0.4%) pushed the total sector’s contribution into negative territory (-0.3%). In addition, a stronger trade-weighted U.S. dollar made U.S. goods and service more expensive overseas, helping to increase the trade deficit by $21.7 billion in 2016 on a year-over-year basis, its highest annual level since 2008. Government investment and consumption added just 0.15% to GDP for 2016, most of which came from state and local governments (0.11%).

Chart 1. Contribution to percent change in real GDP (percent change yr/yr)

The data from Michigan (through Q3) suggest that Michigan’s economy may have increased at a faster rate the nation’s in 2016 (table 2.). Stronger growth is supported by the increased growth in Michigan’s employment in 2016 versus 2015, while the nation recorded a decline in labor growth. Michigan’s demand for labor also increased. . While the civilian participation in the labor force for the nation grew by just 0.1%, Michigan experienced a 1.0% increase in its labor force participation rate in 2016. This helped Michigan’s nonfarm labor force grow by 2.1%, versus 1.8% for the national nonfarm labor force. This is significant because output can increase in one of two ways: increased productivity or increased labor. The stronger growth in labor helps to explain why Michigan’s economy may prove to have grown faster than that of the nation in 2016 once all the data are made available later this year.

Table 2: Michigan Main Economic Indicators

| Indicator | 2014 | 2015 | 2016 |

| Gross State Product 1 | 1.9% | 1.6% | 2.1% |

| Unemployment Rate 2 | 7.1% | 5.4% | 4.7% |

| Participation Rate 2 | 60.5% | 60.3% | 61.3% |

| Nonfarm Job Growth 3 | 78.1 | 63.2 | 90.6 |

| CPI – All Items 4 | 1.0% | -1.3% | 1.7% |

- Year-over-year

- Annual Average

- Annual Average Employment – Y/Y Change in thousands

- Annual Average – Detroit-Ann Arbor-Flint, MI (CMSA)

One of the biggest drivers behind Michigan’s improving employment and economic performance has been the recovery in light vehicles sales, which has set new records for the past two consecutive years, coming in at 17.4 and 17.5 million units for 2015 and 2016, respectively. Almost 20% of Michigan’s GSP currently comes from manufacturing, not counting engineering and technical support, and almost half of Michigan’s manufacturing is in the motor vehicle and parts industry.

For more information on the U.S. and Michigan economies and to see the complete presentation, go to the Recent Presentation tab on the Michigan Economy Blog and click on the February 28 U.S. and Michigan Economic Update.